An accrual is a journal entry that is used to recognize revenues and expenses that have been earned or consumed, respectively, and for which the related cash amounts have not yet been received or paid out.

What is an example of an accrued expense?

Examples of accrued expenses include: Utilities used for the month but an invoice has not yet been received before the end of the period. Wages that are incurred but payments have yet to be made to employees. Services and goods consumed but no invoice has been received yet.

Why do we record accrued expenses?

Since accrued expenses represent a company’s obligation to make future cash payments, they are shown on a company’s balance sheet as current liabilities. … Following the accrual method of accounting, expenses are recognized when they are incurred, not necessarily when they are paid.

What is accrual entry and journal example?

Journal Entry For Accrued Expenses. Accrued expense journal entry is passed to record the expenses which are incurred over one accounting period by the company but not paid actually in that accounting period. Here the expenditure account is debited and the accrued liabilities account is credited.Where are accrued expenses recorded?

You record an accrued expense when you have incurred the expense but have not yet recorded a supplier invoice (probably because the invoice has not yet been received). Accrued expenses tend to be short-term, so they are recorded within the current liabilities section of the balance sheet.

How do you record accrued revenue journal entry?

On the financial statements, accrued revenue is reported as an adjusting journal entry under current assets on the balance sheet and as earned revenue on the income statement of a company. When the payment is made, it is recorded as an adjusting entry to the asset account for accrued revenue.

How do you record accrued expenses on a balance sheet?

Accrued Expenses on Balance Sheet Accordingly, it should be recorded by debiting Wages and Salaries Expenses and crediting Accrued Expenses and by making an offsetting entry by debiting these expenses and crediting Cash when payment is made.

How do Adjusting entries for accrued expenses affect liabilities and expenses?

How do adjusting entries for accrued expenses affect liabilities and expenses? Adjusting entries for accrued expenses can increase liabilities and increase expenses. The financial resources of the government. The individual income tax and Social Security tax are two major sources of the federal government’s revenue.How do I enter an accrued expense in Quickbooks?

- Go to the + New menu and select Bill.

- From the Vendor dropdown, select a vendor.

- From the Terms dropdown, select the bill’s terms. …

- Enter the Bill date, Due date, and Bill no. …

- Enter the bill details in the Category details section. …

- Enter the Amount and tax.

Accrued expenses are expenses a company accounts for when they happen, as opposed to when they are actually invoiced or paid for. An accrual method allows a company’s financial statements, such as the balance sheet and income statement, to be more accurate.

Article first time published onHow do you record expenses in accounting?

- Debit to expense, credit to cash. Reflects a cash payment.

- Debit to expense, credit to accounts payable. Reflects a purchase made on credit.

- Debit to expense, credit to asset account. …

- Debit to expense, credit to other liabilities account.

What is accrued revenue and accrued expense?

Accrued expenses are expenses that are incurred in one accounting period but won’t be paid until another. … Accrued revenues are revenues earned in one accounting period but not received until another.

How do you clear accrued expenses?

Reversing Accrued Expenses When you reverse an accrual, you debit accrued expenses and credit the expense account to which you recorded the accrual. When you post the invoice in the new month, you typically debit expenses and credit accounts payable.

Does QuickBooks do accrual accounting?

Yes, you can simply record your transactions inside QuickBooks as normal. Then, run your reports as Accrual or Cash to show your income or expenses.

How do I set up an accrual in QuickBooks?

- Log in to your file as the Administrator. Make sure you are in Single-User Mode.

- Go to the Edit menu, then select Preferences.

- Select Reports & Graphs, then go to the Company Preferences tab.

- In the Summary Report Basis section, select Accrual or Cash.

- Select OK.

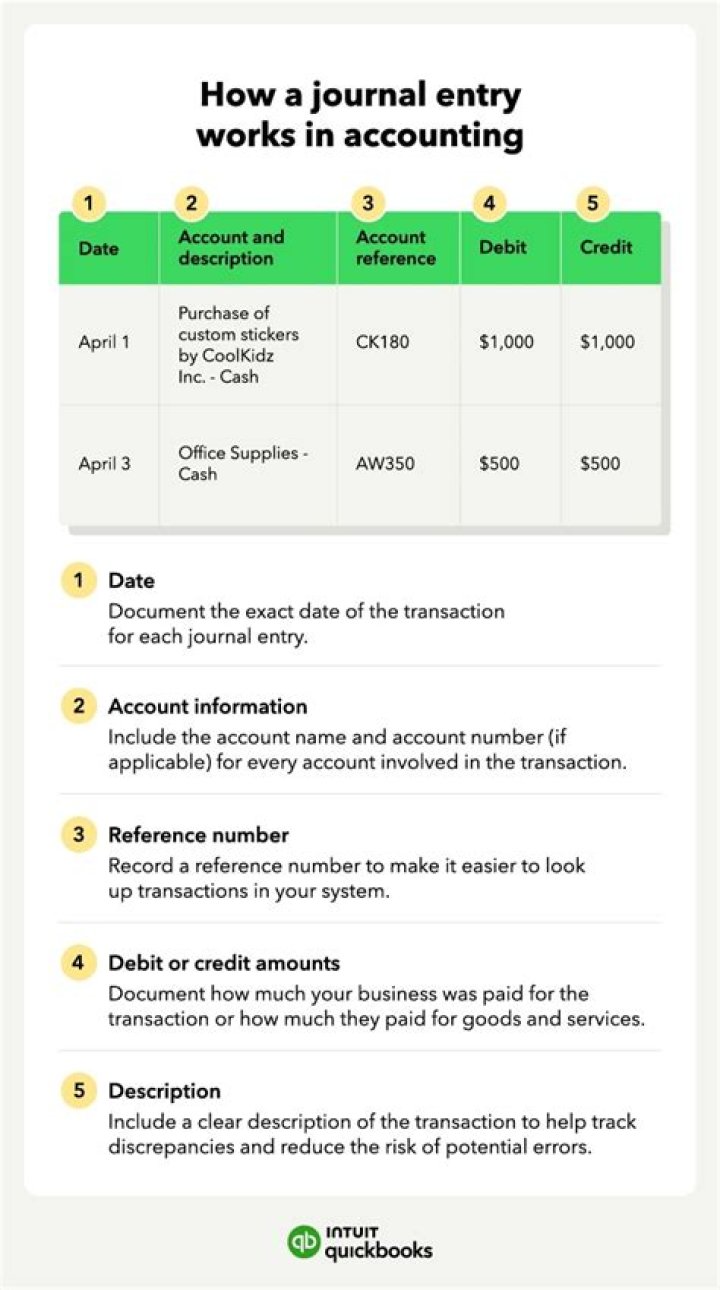

How do you write journal entries in accounting?

- The accounts into which the debits and credits are to be recorded.

- The date of the entry.

- The accounting period in which the journal entry should be recorded.

- The name of the person recording the entry.

- Any managerial authorization(s)

- A unique number to identify the journal entry.

What are the 4 types of adjusting entries?

- Accrued expenses.

- Accrued revenues.

- Deferred expenses.

- Deferred revenues.

Where are expenses recorded in balance sheet?

In short, expenses appear directly in the income statement and indirectly in the balance sheet. It is useful to always read both the income statement and the balance sheet of a company, so that the full effect of an expense can be seen.

When can you accrue an expense?

In short, accruals allow expenses to be reported when incurred, not paid, and income to be reported when it is earned, not received. As examples: A department orders and receives tow computers at the end of June 2004. However, the bill is not received Until July and is not processed until August.

What is the difference between deferred expense and accrued expense?

An accrued expense is a liability that represents an expense that has been recognized but not yet paid. A deferred expense is an asset that represents a prepayment of future expenses that have not yet been incurred.

How is accrued revenue recorded?

Accrued revenues are recorded as receivables on the balance sheet to reflect the amount of money that customers owe the business for the goods or services they purchased. Accrued revenue may be contrasted with realized or recognized revenue, and compared with accrued expenses.

What is reversal journal entry?

Reversing entries, or reversing journal entries, are journal entries made at the beginning of an accounting period to reverse or cancel out adjusting journal entries made at the end of the previous accounting period.