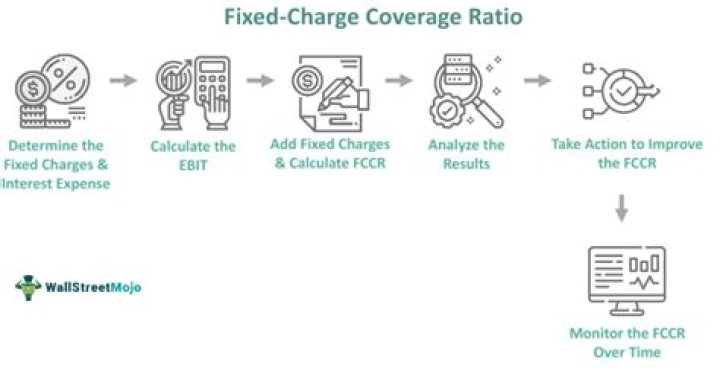

The fixed-charge coverage ratio (FCCR) measures a firm’s ability to cover its fixed charges, such as debt payments, interest expense, and equipment lease expense. It shows how well a company’s earnings can cover its fixed expenses. Banks will often look at this ratio when evaluating whether to lend money to a business.

Is debt service a fixed cost?

Debt Service When businesses have debts in the form of lines of credit or business loans, they must pay to service these debts. The interest that a business must pay on such debts is a recurring fixed cost.

What is debt service coverage requirement?

Debt service coverage ratio – or DSCR – is a metric that measures the borrower’s ability to service or repay the annual debt service compared to the amount of net operating income (NOI) the property generates. DSCR indicates whether or not a property is generating enough income to pay the mortgage.

What does debt service include?

Total debt service: This is just another word for the total amount of debt you pay each year. This would include your estimated new mortgage payment, property taxes, credit card bills, auto loans, student loans and any other payment you make each month. Businesses, of course, take on a wider range of debts each year.Is a high fixed charge coverage good?

Is a High or Low Fixed Charge Coverage Ratio Better? Generally, the higher your FCCR, the better. High FCCRs mean that less of your business revenue is being used to make fixed payments, resulting in more free cash flow, and a greater ability to take on more financial commitments.

Does debt service include principal?

The debt service is the total of all principal and interest paid on debts over the course of a year. For an individual, this includes all debts that are payable in the current year. For a business, it includes interest, any debts maturing within one year, and any principal payments on long-term debts.

Does fixed charge coverage ratio include principal payments?

The fixed charge coverage ratio is similar to the interest coverage ratio. … In terms of corporate finance, the debt service coverage ratio determines the amount of cash flow a business has readily accessible to meet all yearly interest and principal payments on its debt, including payments on sinking funds.

How is debt service calculated?

The annual debt service is the simply the total amount of principal and interest payments made over a 12 month period. … To calculate the debt service coverage ratio, simply divide the net operating income (NOI) by the annual debt.What are examples of fixed costs?

- Rent or mortgage payments.

- Car payments.

- Other loan payments.

- Insurance premiums.

- Property taxes.

- Phone and utility bills.

- Childcare costs.

- Tuition fees.

The debt service concept can apply to the total amount of interest and principal payments associated with all currently outstanding loans (trade accounts payable are not included in the calculation).

Article first time published onWhat is debt service limit?

A debt limit is the maximum debt that the municipality may undertake in a fiscal year. Debt servicing is the maximum amount of principal and interest that the municipality may pay on its debt over the fiscal year. … This amount is also legislated by the provincial government.

Does debt service coverage ratio include line of credit?

Like your business credit score, debt service coverage ratio is an indicator of how likely you are to repay loans, lines of credit and other debt obligations.

Can you have a negative debt service coverage ratio?

A positive debt service ratio indicates that a property’s cash flows can cover all offsetting loan payments, whereas a negative debt service coverage ratio indicates that the owner must contribute additional funds to pay for the annual loan payments.

How do you increase debt service coverage ratio?

- Increase your net operating income.

- Decrease your operating expenses.

- Pay off some of your existing debt.

- Decrease your borrowing amount.

Are taxes a fixed charge?

Summary: Fixed charges are a type of business expense that occurs on a regular basis and is independent of the volume of business. Fixed charge is an umbrella term for a variety of expenses, including principal and interest payments for a loan, insurance, taxes, utilities, salaries, and rent and lease payments.

How do you interpret fixed charge coverage ratio?

- An FCCR equal to 2 (=2) means that the company can pay for its fixed charges two times over.

- An FCCR equal to 1 (=1) means that the company is just able to pay for its annual fixed charges.

How do you increase fixed charge coverage ratio?

- Increase sales in less expensive ways. There are a number of ways to increase a company’s sales without incurring significant costs. …

- Negotiate for a lower rental or lease rates. …

- Refinance loans with high interest rates.

What is a good interest coverage ratio?

Generally, an interest coverage ratio of at least two (2) is considered the minimum acceptable amount for a company that has solid, consistent revenues. … In contrast, a coverage ratio below one (1) indicates a company cannot meet its current interest payment obligations and, therefore, is not in good financial health.

Does fixed charge coverage ratio include depreciation?

A measure of a firm’s ability to meet its fixed-charge obligations: the ratio of (Earnings before interest, depreciation and amortization minus unfunded capital expenditures and distributions) divided by total debt service (annual principal and interest payments).

What is a fixed charge coverage ratio of 4 signifies?

Pre-tax income before lease rentals is 4 times all fixed financial obligations.

What is a good debt service ratio?

A debt service coverage ratio of 1 or above indicates that a company is generating sufficient operating income to cover its annual debt and interest payments. As a general rule of thumb, an ideal ratio is 2 or higher. A ratio that high suggests that the company is capable of taking on more debt.

What type of fund is a debt service fund?

A debt service fund is a cash reserve that is used to pay for the interest and principal payments on certain types of debt.

How do you calculate debt service coverage ratio on financial statements?

The DSCR is calculated by taking net operating income and dividing it by total debt service (which includes the principal and interest payments on a loan). For example, if a business has a net operating income of $100,000 and a total debt service of $60,000, its DSCR would be approximately 1.67.

What are 3 fixed costs?

Common examples of fixed costs include rental lease or mortgage payments, salaries, insurance payments, property taxes, interest expenses, depreciation, and some utilities.

Is bad debt a fixed or variable cost?

Fixed ExpensesVariable ExpensesAmortizationBad DebtTelephoneDelivery FeesInsuranceCommissionsProfessional FeesFranchise Fees

What are 5 fixed expenses?

Examples of Fixed Expenses Rent or mortgage payments. Renter’s insurance or homeowner’s insurance. … Childcare expenses. Student loan or car loan payments.

How do you calculate maximum annual debt service?

The maximum annual debt service is required by borrowing firms from their lenders to gauge their debt capacity. It is used to determine interest and principles on outstanding long-term loans and bond interest and maturing bonds principal. The calculation is made monthly and multiplied by 12 or done over a fiscal year.

Is rent included in debt service?

Asset-based lenders typically calculate the debt service coverage ratio by taking the property’s monthly rent (or expected monthly rent if it’s unoccupied) and dividing it by the monthly debt payment. This includes principal, interest, taxes, insurance, and any association dues (PITIA).

How do you calculate debt service coverage in Excel?

- As a reminder, the formula to calculate the DSCR is as follows: Net Operating Income / Total Debt Service.

- Place your cursor in cell D3.

- The formula in Excel will begin with the equal sign.

- Type the DSCR formula in cell D3 as follows: =B3/C3.

What is NOI in real estate?

Net operating income (NOI) is a calculation used to analyze the profitability of income-generating real estate investments. … NOI is a before-tax figure, appearing on a property’s income and cash flow statement, that excludes principal and interest payments on loans, capital expenditures, depreciation, and amortization.