HUD does not make loans directly – you must use a HUD-approved lender if you’re interested in an FHA loan.

What are the requirements for a HUD loan?

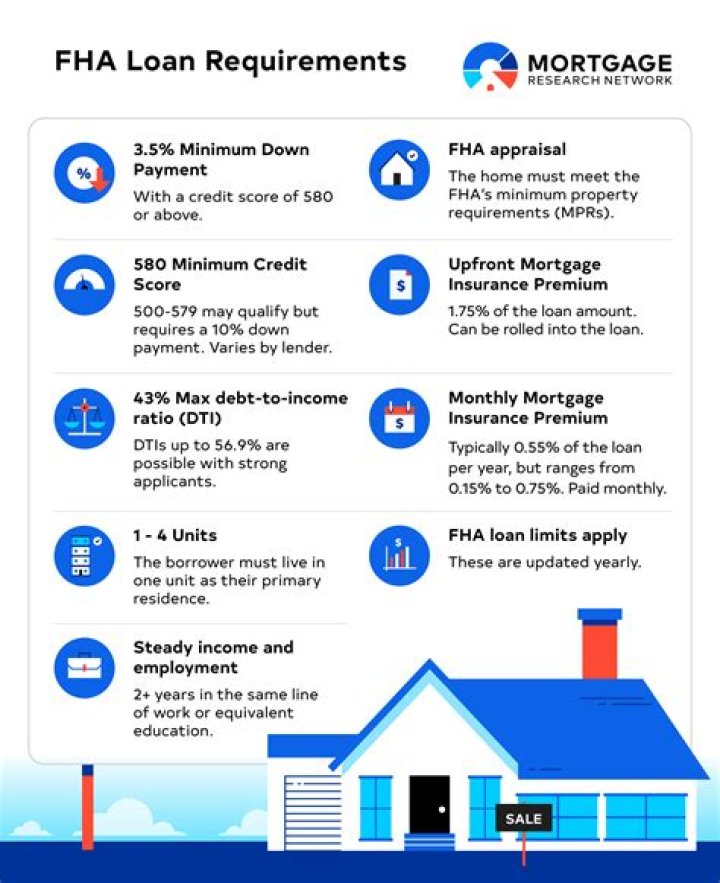

- FICO® score at least 580 = 3.5% down payment.

- FICO® score between 500 and 579 = 10% down payment.

- MIP (Mortgage Insurance Premium ) is required.

- Debt-to-Income Ratio < 43%.

- The home must be the borrower’s primary residence.

- Borrower must have steady income and proof of employment.

What is the minimum down payment for a conventional loan?

The minimum down payment required for a conventional mortgage is 3%, but borrowers with lower credit scores or higher debt-to-income ratios may be required to put down more.

Do you have to buy a HUD home with an FHA loan?

Any qualified buyer can purchase a HUD home. From the FHA official site: “If you have the cash or can qualify for a loan (subject to certain restrictions) you may buy a HUD Home. … While there are FHA guaranteed home loans available for these HUD-owned properties, the government does not guarantee their condition.How does the HUD $100 down program work?

The HUD $100 down program is an FHA loan with a twist. Instead of the minimum required 3.5% of the price down payment, FHA allows a $100 minimum required investment. … In addition to being a HUD owned foreclosure, HUD must state that the listing is eligible for the $100 down incentive.

What is considered a conventional loan?

A conventional loan is a mortgage loan that’s not backed by a government agency. … Conforming conventional loans follow lending rules set by the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac).

What's the difference between FHA and conventional?

FHA loans allow lower credit scores than conventional mortgages do, and are easier to qualify for. Conventional loans allow slightly lower down payments. … FHA loans are insured by the Federal Housing Administration, and conventional mortgages aren’t insured by a federal agency.

Can you put 3 down on a conventional loan?

Can I get a mortgage with 3% down? Yes! The conventional 97 program allows 3% down and is offered by many lenders. Fannie Mae’s HomeReady loan and Freddie Mac’s Home Possible loan also allow 3% down with extra flexibility for income and credit qualification.How long does it take to buy a HUD home?

HUD Preparation Time Once HUD receives a winning bidder’s signed purchase contract it takes seven to 14 days for HUD to sign and return it. Winning HUD owner-occupant bidders then have 45 days from executed contract receipt to close on their homes.

Can you put 5% down on a conventional loan?Downpayment for Conventional Loans: 5% Conventional loans require buyers to make a minimum 5 percent downpayment on a home. Because this is a conventional loan, and because the downpayment is less than twenty percent, private mortgage insurance (PMI) will be required.

Article first time published onWhat are the pros and cons of a conventional loan?

- Competitive interest rates. Mortgage rates hit record lows amid the coronavirus pandemic. …

- Low down payments. …

- PMI premiums can eventually be canceled. …

- Choice between fixed or adjustable interest rates. …

- Can be used for all types of properties.

What is the downside of a conventional loan?

A disadvantage to conventional lending is generally lower debt-to-income ratios are required. Low income and high debt scenarios pose additional risk to private lenders, therefore debt ratio requirements are more stringent with conventional loans.

Can you switch from FHA to conventional?

To convert an FHA loan to a conventional home loan, you will need to refinance your current mortgage. The FHA must approve the refinance, even though you are moving to a non-FHA-insured lender. The process is remarkably similar to a traditional refinance, although there are some additional considerations.

Is a conventional loan good?

A conventional loan is a great option if you have a solid credit score and little debt. You can avoid PMI by paying 20% of the loan upfront, which will lower your mortgage payments. If you’re unable to make a large payment upfront, conventional loans are available with a down payment as low as 3%.

Are conventional loans backed by Fannie Mae?

What Is A Conventional Loan? Conventional loans aren’t insured or guaranteed by a government agency, they’re insured by private lenders. … Conventional loans are also called conforming loans because they conform to Fannie Mae and Freddie Mac standards.

Can you get an FHA loan after a conventional loan?

Scenario one: the borrower has purchased a primary residence with a conventional, VA, or other non-FHA loan and now wants to buy a second property. … FHA borrowers purchasing a home with a single-family FHA mortgage are required to occupy it, usually within 60 days after loan closing.

What can you do with a conventional loan?

- Low interest rates.

- Fast loan processing.

- Diverse down payment options.

- Various term lengths on a fixed-rate mortgage, ranging from 10 to 30 years.

- Reduced private mortgage insurance (PMI)

Who is eligible to buy a HUD home?

Pretty much any “owner–occupant” is qualified to bid on a HUD home for sale – meaning anyone who intends to live in the home full time. There are just two requirements to purchase a HUD home as an owner–occupant: You plan to live in the home for at least 12 months after purchasing it.

What credit score do you need to buy a HUD home?

For those interested in applying for an FHA loan, applicants are now required to have a minimum FICO score of 580 to qualify for the low down payment advantage, which is currently at around 3.5 percent. If your credit score is below 580, however, you aren’t necessarily excluded from FHA loan eligibility.

How hard is it to buy a HUD home?

Buyers interested in FHA loans will need to have a minimum FICO score of 580 to take advantage of the low down payment offer, which can be as low as 3.5% of the purchase price. There are several FHA-sponsored financial assistance and buyer’s programs that can be used to purchase a HUD home.

What is a good credit score for a conventional loan?

Conventional Loan Requirements It’s recommended you have a credit score of 620 or higher when you apply for a conventional loan. If your score is below 620, you might be offered a higher interest rate.

Do conventional loans require PMI?

If you put down less than 20% on a conventional loan, you’ll be required to pay for private mortgage insurance (PMI). PMI protects your lender in case you default on your loan. The cost for PMI varies based on your loan type, your credit score and the size of your down payment.

Is 20 down required for a conventional loan?

What is the minimum down payment required for a conventional loan? Conventional loans require as little as 3% down (this is even lower than FHA loans). For down payments lower than 20% though, private mortgage insurance (PMI) is required. (PMI can be removed after 20% equity is earned in the home.)

Do conventional loans require an appraisal?

One of the main requirements for a conventional loan is that the home must be appraised. The appraiser’s job is to work out the property’s actual market value. Usually, they do this by comparing the property with other, similar homes in the neighborhood that have sold recently.

Can you buy a fixer upper with a conventional loan?

You can certainly buy a fixer-upper with a conventional loan, and many people do, but you’ll still need a plan on how you’ll finance the renovations. … This loan type allows you to combine both the purchase and renovation of the property into one long-term, fixed-rate mortgage.

Why is FHA APR higher than conventional?

FHA rates will be higher than conventional rates when the borrower has low credit scores. Although FHA loans are helping to make home ownership more affordable, low credit scores signal high risk to FHA lenders. As a result, they impose interest rate adjustments based upon the credit score of the borrower.

Is a conventional mortgage a fixed mortgage?

A “fixed-rate” mortgage comes with an interest rate that won’t change for the life of your home loan. A “conventional” (conforming) mortgage is a loan that conforms to established guidelines for the size of the loan and your financial situation.

How do I get rid of PMI on an FHA loan?

Getting rid of PMI is fairly straightforward: Once you accrue 20 percent equity in your home, either by making payments to reach that level or by increasing your home’s value, you can request to have PMI removed.

How do I get rid of my PMI?

To remove PMI, or private mortgage insurance, you must have at least 20% equity in the home. You may ask the lender to cancel PMI when you have paid down the mortgage balance to 80% of the home’s original appraised value. When the balance drops to 78%, the mortgage servicer is required to eliminate PMI.

What's the PMI on an FHA loan?

With an FHA mortgage, you’ll also pay a monthly mortgage insurance premium (MIP) of 0.45% to 1.05% of the loan amount based on your down payment and loan term.